A specific Sales Tax rate eg. If withholding tax 10 is to be applied on above transaction then.

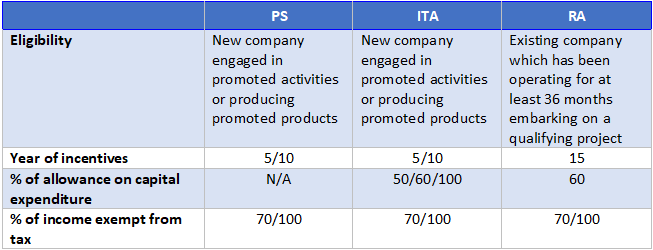

Tax Incentives In Malaysia Industry Malaysia Professional Business Solutions Malaysia

The following countries have concluded double tax treaties with Malaysia.

. WHT Dividends 1 Interest 2 Royalties 3a 3b Special classes of incomeRentals 4 5 Resident corporations. Malaysia has entered into more than 60 bilateral DTAs. The Malaysian Inland Revenue Board MIRB has now issued its FAQs to provide further clarification on the application of Section 107D with the following notable points-.

Assuming that the foreign service provider is based in Singapore if the service is considered under Special Classes of Income eg. Withholding tax means an amount representing the tax portion of an income of a non-resident recipient withheld by the payer in Malaysia. The tax withheld must be paid to the Internal Revenue Department IRD within fifteen days from the date of withholding.

For example A engages B who is a foreign consultant to give consultation on a project and pays 100000. Income Tax Act 1967. Introduction to Withholding Tax.

Gross amount 1000 net amount 200 tax 1200. As we know WTH tax percentage is applied on gross amount. The WHT is not applicable on payment in the form of credit note and discount given to ADDs and contra-transaction with ADDs.

Company N is a foreign company providing services to a Malaysian company called. The withholding tax in Malaysia is an amount withheld by the party making payment payer on income earned by a non-resident payee. Any person making the following payments is required to withhold income tax at the time of payment at the rates listed below.

Company purchases raw material from vendor of 1000 with 20 input tax. These DTAs commonly provide for either an exemption or reduction in the prescribed rate for certain types of withholding taxes. Example 1 Syarikat Maju Sdn Bhd a Malaysian company signed an agreement with Excel Ltd a non-resident company to provide a report addressing the industry structure market conditions and technology value for the Multimedia Super Corridor Grant Scheme.

For taxpayers that have the digital certificates for individual files SG or OG or the digital certificates for company files OeF- file C they can now pay withholding taxes under form CP37A electronically to IRBM via e-WHT. Be subject to both imported services and withholding tax for example services performed in Malaysia by a third-party foreign service provider. 030 Malaysian ringgits MYR per litre is applicable.

Combination 3 above does not tantamount to double taxation as withholding tax is in principle a tax imposed on the income of the non-resident provider while service tax is a tax on consumption by. Applicability of Section 107D WHT. Ltd the withholding tax on interest income rate is 10 of the interest as the company is.

Corporations making payments of the following types of income are required to withhold tax at the rates shown in the table below. Company N is a foreign company providing services to a Malaysian company called Company M. The gross amount which.

Section 107A 1 a 107A 1 b 10 3. Let us assist you to demystify the changes made to the withholding tax provisions and support you in complying with your withholding. However if it is proven otherwise the withholding tax on services is exempted under Income Tax ExemptionNo9 Order 2017.

In the case of Mochiko Co. Of that 1500 parts of it goes to state income tax federal income tax unemployment and Medicare liabilities. Example of Withholding Tax.

Withholding tax is an amount withheld by the party making payment payer on income earned by a non-resident payee and paid to the Inland Revenue Board of Malaysia. Under the S109B Income Tax Act 1967 A would need to withhold 10 of that. The payer has to make the payments based on the table below.

Income is deemed derived from Malaysia if. Form CP37A Pin 52017. Individuals except 1099 employees can easily look.

Quoting directly from the Inland Revenue Board of Malaysias official website withholding tax is an amount that is withheld by the party making payment payer on income earned by a non-resident payee and paid to the Inland Revenue Board of Malaysia IRBM. Payer refers to an individualbody other than individual carrying on a business in Malaysia. Though he earns 6000 a month his employer withholds 1500 from his paycheck leaving 4500 for John.

Based on Example 2 of the guidelines payment for online service via a platform to non- resident is subject to withholding tax under Section 109 of the Act if the services are performed in Malaysia. Typically the withholding tax on interest income rate is fixed at 15 of the aforesaid. For example the DTA between Malaysia and Singapore reduces withholding tax rate in respect of royalties and technical fees to 8 and 5 respectively.

What is withholding tax. Corporate - Withholding taxes. Withholding tax is an amount withheld by the party making payment payer on income earned by a non-resident payee and paid to the IRB.

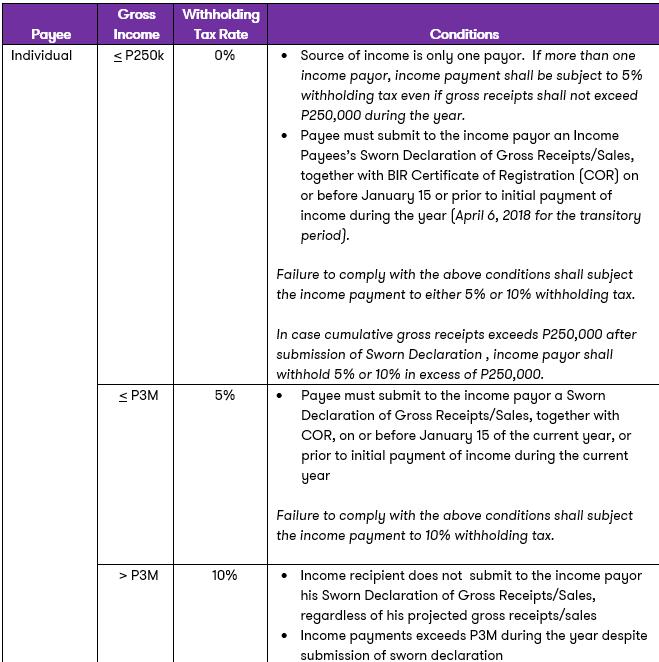

See Note 5 for other sources of income subject to WHT. Tax withheld from payments to residents and branches registered in. To withholding tax has been redefined effective 17th January 2017 resulting in significant broadening of the scope of payments to which the withholding tax applies.

Payments for technical advice assistance or services is subjected to withholding tax including any portion of work done outside Malaysia. Goods which are subject to 5 percent Sales Tax include certain food prepared fruits vegetables and meats printers and mobile phones. Net amount 1000 and tax amount 200.

With that being said the government of Malaysia has formed treaties where its withholding tax on interest income can be lower than 15. This amount has to be paid to LHDN. Lets say Johns yearly salary is 72000.

As the name goes Withholding tax means an amount representing the tax portion of an income of a non-resident recipient withheld by the payer in Malaysia and paid directly to the Inland Revenue Board of Malaysia. He is required to withhold tax on payments for services renderedtechnical advice. Any tax resident person who is liable to make certain specified types of payments to a non-resident is required to deduct withholding tax at a prescribed rate applicable to the gross payment and remit it to the Malaysian IRB within one month of paying or crediting.

This form can be downloaded and submitted to Lembaga Hasil Dalam Negeri Malaysia. The withholding tax provisions under the Act place tremendous demand on payers and hence a good understanding of the Malaysian withholding tax regime is critical to avoid any potential on non-compliance penalties. WTH tax 10 on gross amount 10 on 1200 120.

Malaysia is subject to withholding tax under section 109B of the ITA. Technical Fees it will. An individual body company carrying on business in Malaysia.

Goods exempted from Sales Tax include basic food eggs vegetables cereals pharmeceutical products and steel products.

Chapter 8

Bbva Bank Statement Template Mbcvirtual Statement Template Bank Statement Templates

New Withholding Rules On Payments Of Professional Talent And Commission Fees Grant Thornton

Media Resources Downloads Pembangunan Sumber Manusia Berhad Exemption Of Levy Order 2001 Kwsp 3rd Schedule 7 For Period Apr 2020 To December 2020 Gst Income Tax Forms Gst Forms Epf Kwsp Forms Socso Perkeso Forms News

Cukai Pendapatan How To File Income Tax In Malaysia

Monthly Budget Worksheet Simple Monthly Budget Template Simple Monthly Budget Temp Budgeting Worksheets Monthly Budget Worksheet Printable Budget Worksheet

Tax Incentives In Malaysia Industry Malaysia Professional Business Solutions Malaysia

Chapter 4 B Employment Income

Details Of 2 Agent Commission Withholding Tax L Co

Chapter 8

Payments That Are Subject To Withholding Tax Wt

Procuring Service From Foreign Providers Here S An Additional 6 Tax Accountants Today

Tax Incentives In Malaysia Industry Malaysia Professional Business Solutions Malaysia

Chapter 8

Chapter 8

Updated Guide On Donations And Gifts Tax Deductions

Chapter 8

Chapter 8

Tax Alert Grant Thornton Malaysia

- jalan kereta api sabah

- proton saga 2018 merah

- plastik biru construction tapak

- batu garnet merah tua

- kesan tarik rambut anak

- j force jack biru

- harga cermin mata korea style lazada

- cermin mata brand korea

- resepi kuah ayam percik merah

- pos malaysia international hub (klia)

- unifi package for business

- lanskap rumah banglo

- undefined

- second hand luxury handbags malaysia

- hsbc log on malaysia

- jual kereta 4x4 malaysia

- withholding tax malaysia example

- cover set 135 lc biru

- bintik merah berair di badan

- tema hari pekerja 2019